The Plans – A Conversation on the Affordable Care Act

________

Court ruling in GOP case puts health security for millions in jeopardy – MSNBC

__________

___________

Obamacare’s individual mandate, the new target in the GOP tax plan, explained – Vox

__________________________

-

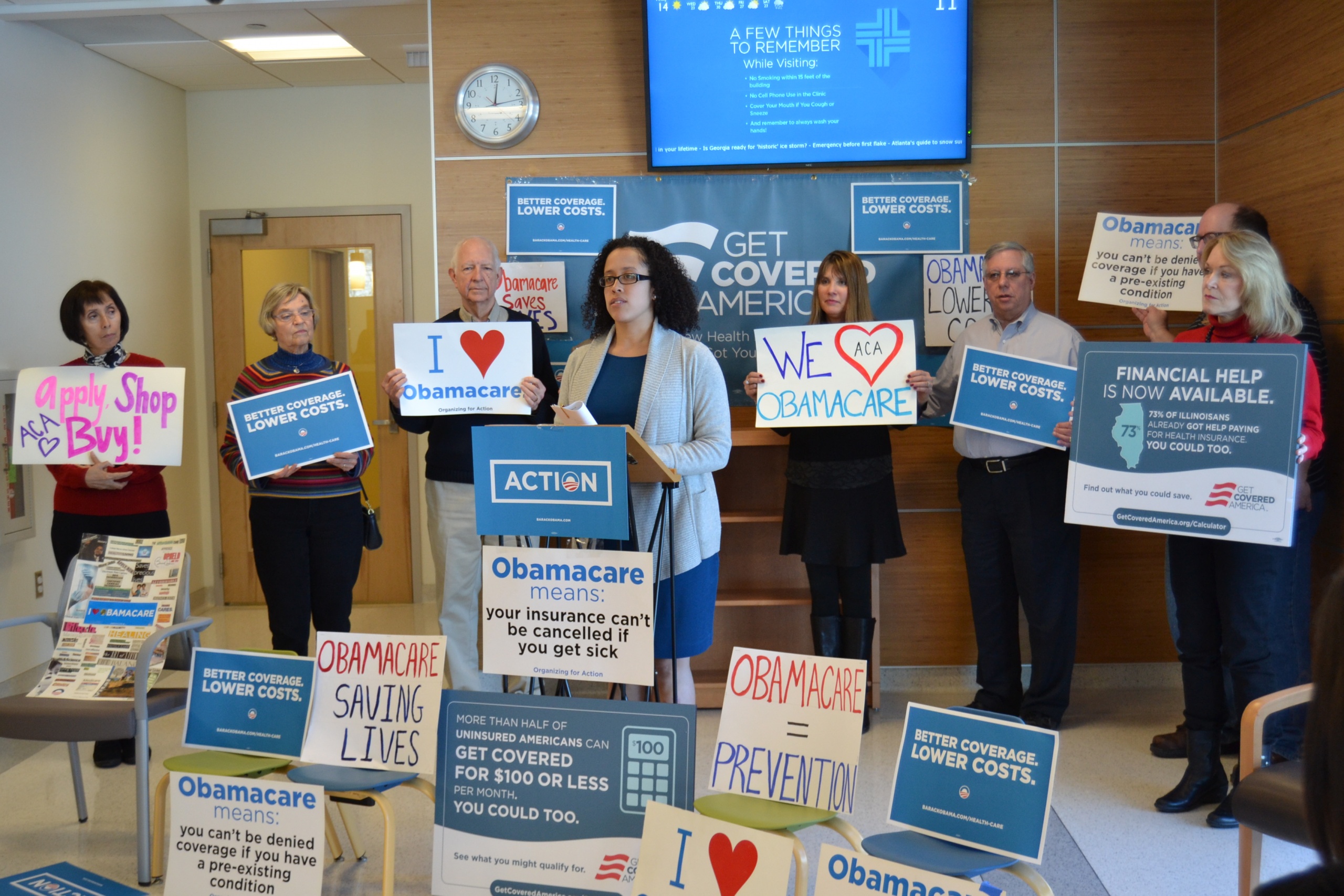

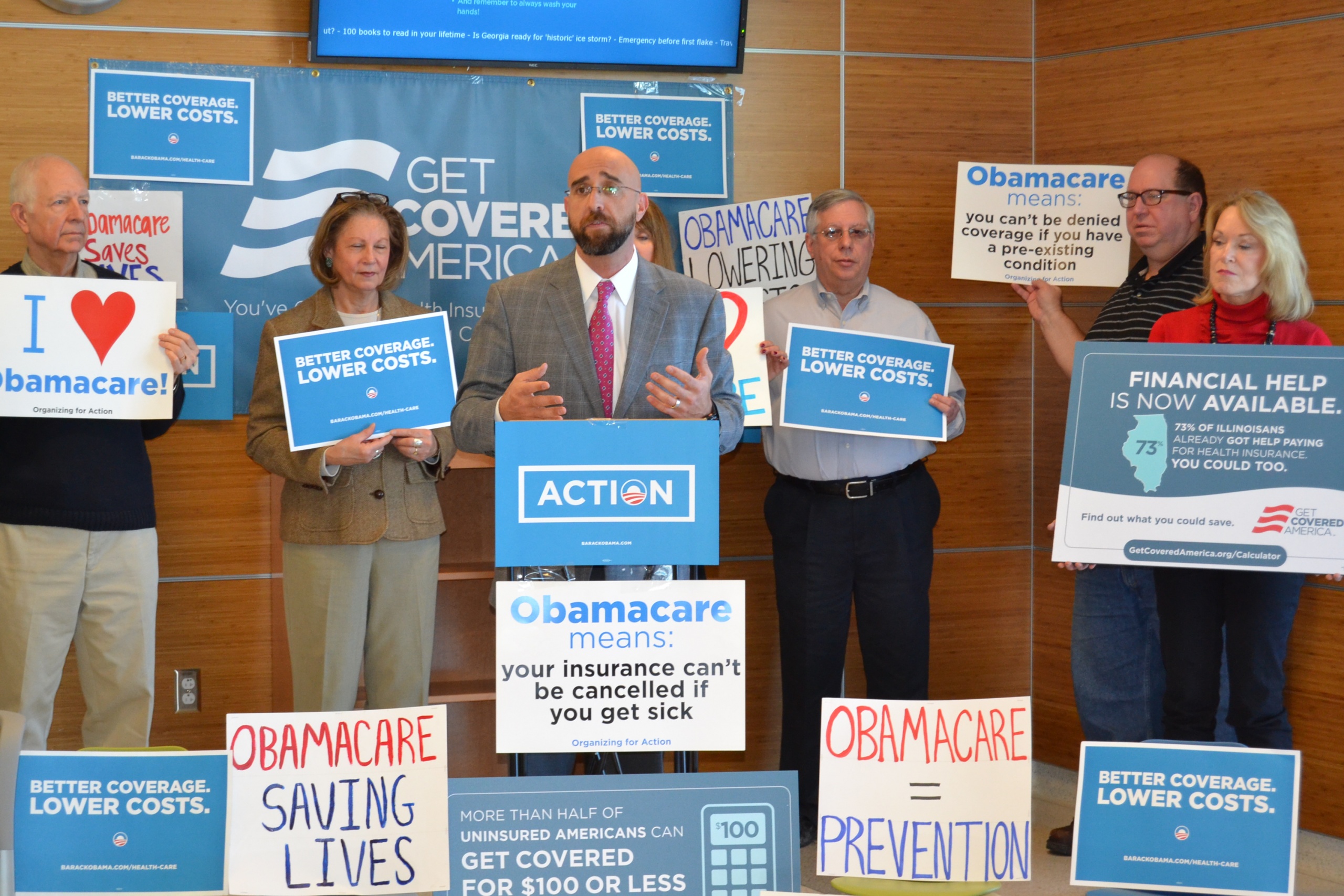

Governor Rauner Vetoes Legislation to Safeguard Key Healthcare Protections

This week, Gov. Bruce Rauner vetoed two key pieces of legislation designed to safeguard the protections of the Affordable Care Act: HB 2624, which would have put limits on short term health insurance plans, which provide weaker protections under the false guise of more affordable coverage; and HB 4165 which would have required a resolution from the General Assembly for Illinois to use a federal waiver to reduce healthcare access.

See Protect Our Care Illinois’ statement and action steps. Stay tuned for more news as we try to secure overrides to these vetoes.

____________________

Understanding the Affordable Care Act

If you are not sure how the loss of the Affordable Care Act would affect your life, click on the link below for a comprehensive explanation from OFA National.

https://www.ofa.us/obamacare/

___________

What can you do?

Actions and Resources for New Volunteers

-

How can you stay updated about OFA…Join our OFA Monthly Volunteer Call — registration link

-

-

-

On the first Monday of each month, this call is open to all volunteers and will serve as a place to get updates from OFA on our issues. If you are interested in getting more information about the work we are doing, please join the call.

-

-

-

-

-

-

As our communication tool, new volunteers and supporters should join Connect to share best practices, brainstorm ideas and tout their successes. It’s also the place where we can update folks about upcoming events & actions, share relevant policy updates, etc.

-

-

-

-

-

Join us on social media

-

-

TW: @OFA

-

-

-

-

Join the Truth Team — get the facts and help spread the truth

-

Actions YOU can take:

-

This is an entry point for those who want to learn more about how they can get involved in defending Obamacare.

-

Note: this will be very similar to the previous briefing call we had on January 11

-

-

-

Join the Defend Obamacare Briefing Call — Thursday, January 26

-

-

-

Use the call tool — phone your elected official tell that repealing Obamacare is irresponsible and affects real lives

-

-

-

Join in by finding an OFA event in their area — there are still community action meetings planned through January as well as Defend Obamacare events happening across the country

-

-

Share their story of how Obamacare has helped them or friends/family member by submitting to acaworks.org.

-

_________________

Yes, You Can Still Enroll in Obamacare: Five Answers to Questions About Getting Covered By HAEYOUN PARK OCT. 14, 2017 – NYT

_____________________

How to Fight the New Trumpcare – Opinion New York Times

_____________________

TESTAMENT TO HOW THE AFFORDABLE CARE ACT SAVES LIVES…

My name is Karah. I’m 34. I’m a caregiver and mother of one. Last year, early spring, I was very excited because I thought I was carrying a long awaited second child. Two months later, I lost the baby, but I didn’t recover. I got worse. I was throwing up as many as 10 times a day. I was catching every virus possible. I went to the doctor and was told that parts of the pregnancy were still growing and it wasn’t a baby. I would need surgery.

Luckily I got on Washington Apple Health and was supported by the ACA. The doctor was afraid to wait 2 days before putting me in for surgery. I didn’t have to choose between my life and my family’s financial future. My insurance saved my life and I had surgery in less than 48 hours. But it wasn’t over.

Two weeks later the doctor told me it was still growing and was now officially considered a molar pregnancy. I was sent to a new doctor who specializes in “cancerous uterine growths.” Because I hadn’t ignored my health, because my insurance had allowed me to take care of my self and my family, I was only stage one. “Good news,” they said, “because you’re stage one, we only have to inject you with the lowest dosage of radioactive death in the hopes it kills your disease before it or the disease kills you.” (I paraphrase.)

So began 6 months of being injected with death to save my life, incuding a fantastic helicopter ride after loosing over a quart of blood in less than 3 hours. Praying that my liver would hold out, that I could eat that day, that I would be alive next year. I continued to work. I continued to smile. I continued to fight. And I continued to live.

I’m a survivor. I’m here today for my son, family, and friends because I went to the doctor as soon as something was wrong. I’m here because ACA paid my doctors to save my life.

Health insurance is more important than you think. Health insurance is having your mother, your sister, your best friend by your side. Thank you ACA and former President Obama for giving me the chance to be here with all of the people I love.

_______________

|

|||

|

___________________

Senate Republicans Are Closer Than Ever To Repealing Obamacare – HuffPost

____________________

-

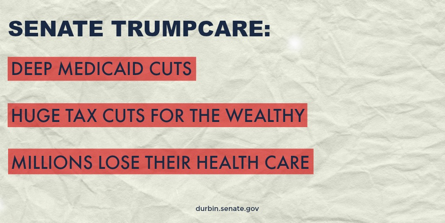

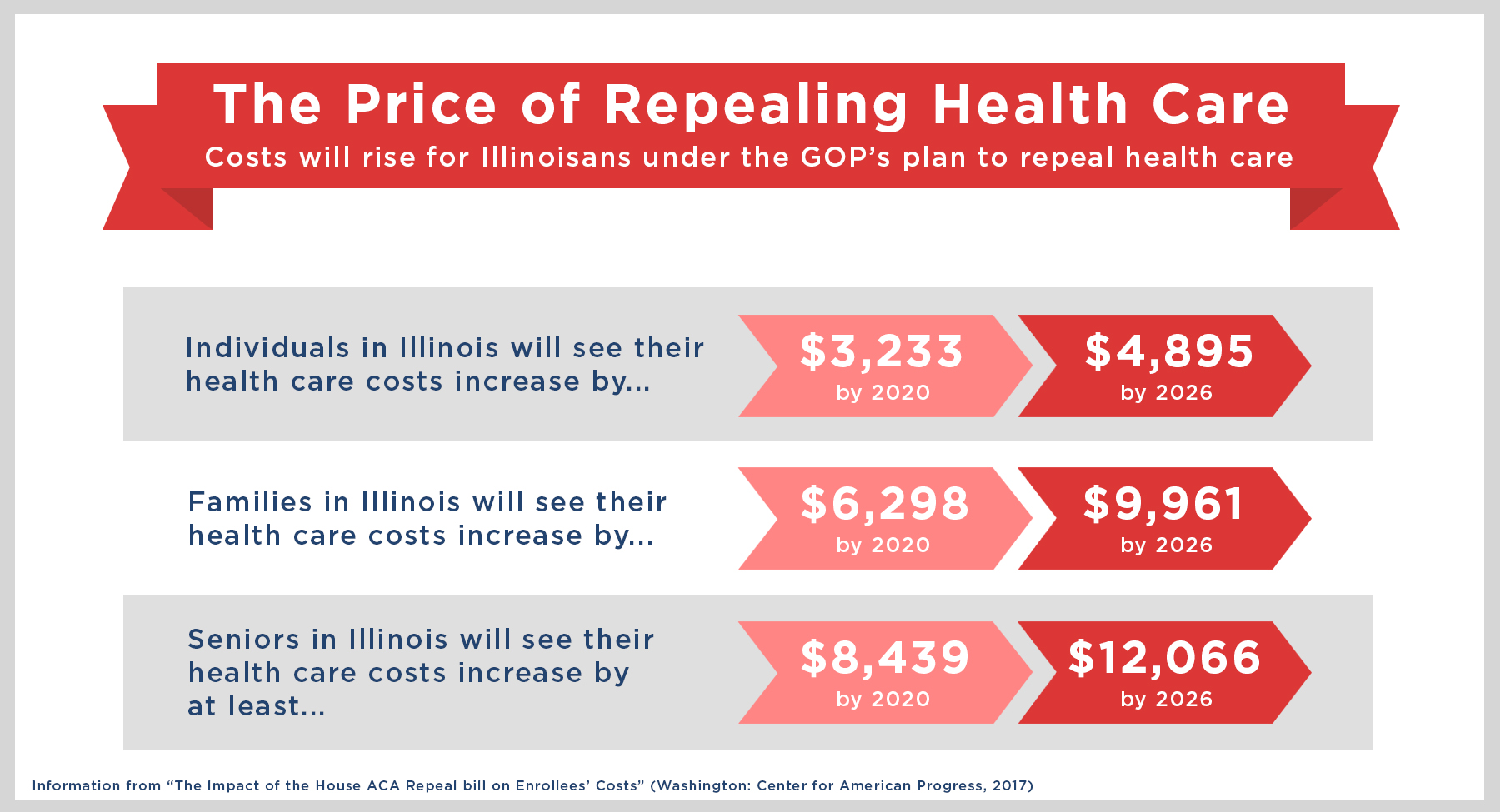

Fellow Illinoisan, Though the news in Washington is dominated by almost daily bombshell revelations about President Trump’s scandal-plagued White House, it is critically important for every Illinoisan to understand what exactly the Republican plan to repeal health care would mean for them. That is why, earlier this year, I released a report – “TrumpCare: Less for More, An Analysis of the Impact of Repealing the Affordable Care Act on Illinois ” – that details what our state stands to lose if President Trump and Congressional Republicans are successful in passing their legislation to repeal the Affordable Care Act (ACA).

Read my report to learn what Illinoisans stand to lose if Trumpcare becomes the law of the land.

After requesting information from every hospital, public health department, and major medical society in the state, the report summarizes how the ACA has helped individuals, families, and providers in all 18 Illinois congressional districts, and provides information on the increased out-of-pocket costs and number of people in each congressional district that stand to lose health coverage or benefits under the House-passed Republican repeal bill.

Republicans’ plan to repeal health care would mean deep cuts to Medicaid, higher premiums for seniors, low- and middle-income families and rural communities, loss of protection for people with pre-existing conditions, and cuts to mental health and substance abuse treatment options—all to pay for a huge tax giveaway for big businesses and the super rich. Next year alone, the bill would cause hundreds of thousands of Illinoisans to lose their health coverage. This repeal bill would have devastating impacts on cities and towns across Illinois – that is why my colleagues and I are working so hard to defeat it.

Sincerely,

Dick Durbin

United States Senator - TrumpCare Less for More – Senator Dick Durbin – March 23, 2017

- Former health law adviser: Seniors will feel the pinch if ACA repealed – The Axe Files

- The Future of Healthcare – Institute of Politics at the University of Chicago

- Republicans’ ACA Replacement Proposals Fall Short of Providing the Protections and Care People Currently Enjoy Under the Affordable Care Act – Families USA

- Pediatrician discusses arrest at Roskam protest in Palatine – Daily Herald

- Grading Obamacare: Successes, Failures and ‘Incompletes’ – New York Times

-

January 30 – February 3, 2017

In light of recent discussions over the future of the Affordable Care Act (ACA or “Obamacare”), we released a new chartbook highlighting some of the major issues and considerations for “repeal and replace.” Our chartbook provides an overview of the health care system today, focuses on the implications of “repeal and replace” on the federal budget as well as health care costs, coverage, Medicare solvency, and an array of other issues.

Experts Discuss Obamacare “Repeal and Replace“

This week, we co-hosted an event with the Kaiser Family Foundation (KFF) on the “Major Considerations for Repealing and Replacing the Affordable Care Act.” The event convened two expert panels discussing the principles, options, trade-offs, and implications of any plan to replace the Affordable Care Act, including an in-depth conversation on what replacement pieces might look like. Panelists included Stephanie Carlton, Liz Fowler, Harold Pollack, Avik Roy, Marc Goldwein, Joseph Antos, Bill Hoagland, Chris Jennings, Peter Lee, and Larry Levitt.

A full video of the event is available.

Following up on last week’s Congressional Budget Office (CBO) Budget and Economic Outlook, we took deeper dives into what CBO’s newest projections indicate for the long term, achieving fiscal goals, and how alternative policies could affect it. Debt will continue to rise over the next 30 years, reaching up to 145 percent of Gross Domestic Product (GDP) by 2047. The outlook also indicates reaching levels of fiscal sustainability are now even harder, with savings needed to balance the budget within a decade rising to over $8 trillion. And if policymakers continued to pass tax and spending measures without paying for them, an additional $2 trillion over the decade would be added to the debt.

- Another Warning Sign For Republicans Trying To Repeal Obamacare Now the AARP is making noise.

- Progressive activism takes its toll on congressional Republicans – Rachel Maddow Show

- Rep. Roskam’s office cancels Obamacare meeting when reporter shows up – Chicago Tribune

- Illinois to Congress: Be cautious on repeal of health care law

- Health Law Repeal Could Cost 18 Million Their Insurance, Study Finds – NY Times

-

January 17, 2017Policymakers are expected to soon consider legislation to repeal and possibly replace large parts of the Affordable Care Act (“ACA” or “Obamacare”). Any significant changes to the ACA are likely to have substantial impacts on health care costs, insurance coverage, premiums, the distribution of benefits, economic growth, and the federal budget.Because the ACA included a mix of spending increases, spending reductions, and tax hikes, the magnitude and direction of the budgetary impact of “repeal and replace” legislation is highly dependent on yet-undetermined details (see our estimates of some illustrative scenarios here).With the national debt at post-WWII era record-high levels and growing unsustainably, it is important that changes to the ACA be fiscally responsible. We recommend that any repeal and replace legislation – whether enacted all at once or in pieces – follow these guiding principles:1. Retain or replace, and build upon, the ACA’s cost-control measures.2. Reduce, rather than increase, the debt.3. Maintain or improve Medicare solvency.It appears some policymakers would prefer to enact ACA repeal and replacement in pieces, with the first part (“repeal and delay”) setting a future date for the ACA’s coverage provisions to expire. This approach is not optimal. But if it is pursued, repeal and delay should not only abide by the principles above but also the following additional principles:4. Continue the ACA’s offsets as long as coverage provisions are retained.5. Generate sufficient repeal savings to finance any future replacement.6. Enact any replacement in a timely and fiscally responsible manner.

Legislation that fails to meet these goals would likely lead to higher debt, a less secure Medicare program, and ultimately slower economic growth.

1) Retain or replace, and build upon, the ACA’s cost-control measuresCombined federal health care spending is the largest part of the federal budget. It is also the fastest growing part aside from interest. Repeal and replace legislation should therefore focus on controlling health care cost growth; at minimum, it should retain the parts of the ACA designed to do just that.As recently as 2000, federal health spending totaled 3.1 percent of Gross Domestic Product (GDP). Today, it costs 5.5 percent of GDP. And based on Congressional Budget Office (CBO) projections, we estimate it will grow to 6.7 percent of GDP within a decade and 9 percent within thirty years. Though this growth is in part due to the population aging, it is also due to per-capita heath care costs continuing to grow faster than inflation or the economy, which impacts not only the federal government but also state and local governments, businesses, and households.Health care cost control is hugely important. Over the next three decades, CBO projects per-capita health care spending to grow about 1 percentage point faster than the economy each year, on average. If policymakers successfully slowed its growth to the pace of the economy, debt in three decades would rise to slightly over 100 percent of GDP, rather than roughly 140 percent. On the other hand, if health costs grew 2 percentage points faster than GDP per capita, debt would rise to over 190 percent of GDP.Although many parts of the ACA likely accelerated health care cost growth, many other parts – particularly those addressing Medicare – were designed to slow cost growth.In particular, the ACA included:-

“Productivity adjustments,” which limit the growth of Medicare provider payments in order to encourage more cost-effective delivery of care.

-

Payment reforms and experiments designed to reduce hospital readmissions, increase the use of comparative effectiveness research, encourage care coordination, and begin to replace fee-for-service with new models such as bundled payments and Accountable Care Organizations (ACOs).

-

New government entities charged with developing and testing new payment reforms (the Center for Medicare & Medicaid Innovation) and limiting Medicare cost growth (the Independent Payment Advisory Board, or IPAB).

-

Demonstration projects to test mechanisms for better coordination of Medicare and Medicaid enrollees who are eligible for both programs, including managed care for long-term services and supports, multi-payer arrangements, and behavioral health integration.

-

A “Cadillac tax” on high-cost insurance plans designed to slow the growth of health spending resulting from employer-provided health insurance.

Many of these provisions are still in their infancy, though some are already proving effective in helping to stem health care cost growth. For the most part, they should be retained and built upon under any repeal and replace plan. For example, policymakers could adopt recommendations we made in 2015 to significantly expand ACOs and bundled payments.Policymakers may wish to repeal some of the ACA’s unpopular cost-control measures. If repealed, these provisions should be replaced with others that are at least as effective. For example, if the Cadillac tax is repealed it could be replaced with a limit on the tax exclusion for employer-sponsored health insurance. If IPAB were repealed, it could be replaced with a “Medicare trigger” that limits Medicare cost growth by encouraging congressional action and making automatic changes (for example, payment freezes) if action fails.Repeal and replace proposals should be viewed as an opportunity to enact further cost controls on top of those in the ACA. These could include, for example, modernizing Medicare cost-sharing, limiting Medigap plans, reforming medical malpractice rules, reducing costs through more market competition, or encouraging the use of low-cost drugs.While the debate over repeal and replacement is likely to revolve largely around coverage, it is important that policymakers remember cost control is the key to sustaining any reforms over the long run.2) Reduce, rather than increase, the debtRepeal and replace legislation – whether enacted in a single bill or across multiple bills – should aim to reduce the near- and long-term projected debt. Certainly, health reform should not be adding to the national debt, which is already higher as a share of GDP than at any time other than just after World War II.Repealing the ACA in its entirety would cost $350 billion ($150 billion on a dynamic basis) over ten years, but even retaining all of the ACA’s Medicare savings would only generate $750 billion ($950 billion, dynamic) of savings. $750 billion may prove insufficient to pay for replacement legislation, considering that the ACA’s coverage provisions cost $1.55 trillion on net ($1.75 trillion, dynamic) and close to $2 trillion when removing savings from the individual and employer mandates. See our full paper “The Cost of Full Repeal of the Affordable Care Act” for more discussion of these scenarios.Ensuring repeal and replace legislation reduces the deficit will likely require policymakers to retain most health and revenue offsets from the ACA, or else replace them with alternative savings measures, while ensuring any replacement is cost-effective and affordable.Policymakers should especially focus on ensuring legislation reduces the long-term debt over the next few decades, as the baby boom generation retires. By our estimates, repealing the coverage and revenue provisions would save roughly $1.5 trillion over two decades, while repealing only the coverage provisions would save about $3.5 trillion. And repealing the entire ACA would cost nearly $4 trillion over two decades.Over the long term, savings from repeal should be larger than the cost of replacement.3) Maintain or improve Medicare solvencyWhile much of the focus around the ACA is on the exchange subsidies and Medicaid expansion, the law also made significant changes to extend the solvency of Medicare Part A’s Hospital Insurance (HI) trust fund. Though these initial improvements were made in part by “double counting” some savings, policymakers should nonetheless avoid backtracking and thus worsening the state of the HI trust fund.The ACA strengthened the HI trust fund in two ways. First, it increased the revenue going into the trust fund through a 0.9 percent HI payroll surtax on high earners. At the same time, it reduced the growth of Medicare spending by reducing reimbursements to Medicare Advantage plans, slowing the growth of provider payments, and enacting other reforms.By our estimates, full repeal of the ACA – including the Medicare cuts – would advance the HI insolvency date from 2026 to 2021 and triple its 10-year shortfall. Repealing the coverage and revenue provisions while retaining the Medicare cuts would advance the HI insolvency from 2026 to 2024 and increase the 10-year shortfall by about half.Policymakers should preserve and build upon the Medicare solvency improvements. This could be accomplished most easily by maintaining all of the Medicare reductions and the HI surtax in the ACA. But even if policymakers decide to repeal the ACA in full, these provisions should be replaced with alternative improvements.Repeal and replace legislation should also maintain or improve the financial sustainability of Medicare Part B and Part D, though those programs do not rely on trust fund financing in the same way Medicare Part A does.Repeal and delay must meet additional standardsWhile many health experts believe ACA repeal and replacement should be enacted concurrently, some policymakers argue they should be enacted in parts. The “repeal and delay” strategy would repeal large parts of the ACA at some point in the future – perhaps after two or four years – with the intention of enacting an ACA replacement before that time frame passes.Separating “repeal” from “replace” legislation introduces a number of challenges, many beyond the scope of this paper. From a fiscal perspective, timing issues might be used to obscure the costs or savings; repeal and delay legislation might make it more difficult to pass fiscally responsible replacement legislation.To ensure health reform is fiscally responsible, repeal and delay would need to conform with the three principles above as well as the additional principles below:4. Continue the ACA’s offsets as long as coverage provisions are retainedThe previous version of repeal and delay, vetoed by President Obama in January 2016, would have repealed the ACA’s mandates and revenue provisions immediately while delaying repeal of its insurance subsidies and Medicaid expansion for two years. Such an approach would add to near-term deficits and would likely reduce long-term deficits in name only.We estimate under an approach like this that a two-year delay would cost roughly $50 billion over two years, while a four-year delay would cost $135 billion over those four years. In this case, the $450 to $600 billion of gross savings in subsequent years would not only have to pay for a replacement, but also cover the cost of repeal in the early years. Adding to near-term deficits for this purpose would be unjustified and unwise. (See “Repeal and Delay Shouldn’t Increase Near-Term Deficits“ for more detail.)Delayed repeal should mean delay for all parts of repeal, not just the coverage provisions. Retaining the ACA’s giveaways while repealing its offsets – even on a temporary basis – represents irresponsible budgeting that could prove costly in the future. So long as policymakers continue to offer costly coverage provisions, they must keep all the measures paying for that coverage. Better yet, policymakers should retain all of the offsetting provisions until a replacement is put in place.5. Generate sufficient repeal savings to finance any future replacementIf policymakers retain the ACA’s Medicare savings, repeal and delay legislation by itself is likely to reduce budget deficits. By our estimates, repealing all mandate and revenue provisions immediately and coverage provisions after two years would save $550 billion over a decade; repealing coverage provisions after four years would save $300 billion.However, if replacement legislation is expected to follow repeal, simply reducing the deficit in repeal is not enough. Instead, repeal legislation needs to reduce the deficit by enough to fully finance the net cost of any future replacement legislation. Since consensus replacement legislation has not yet been written, it is impossible to know the cost of any new coverage provisions nor the savings from new offsets and thus what is needed to pay for the difference. Given this reality, it is best to follow the guideline that “more is better” and generate as much savings as possible in the repeal and delay legislation. If a replacement bill ends up being less expensive than the savings from repeal, leftover funds could be dedicated to deficit reduction.6. Enact any replacement in a timely and fiscally responsible mannerThe longer policymakers wait between repealing the ACA and replacing it, the more disruptions and uncertainties will be created for individuals seeking coverage, companies, and providers – not to mention the additional cost and fiscal implications. Maintaining coverage with no individual mandate and a set of exchanges slated to disappear will likely require spending more on insurance companies so they continue to offer coverage and more on individuals who will be facing higher premiums and thus larger subsidies. Yet replacing the ACA with an even costlier plan would worsen an already unsustainable fiscal situation.Upon repeal, policymakers should act quickly to develop, agree to, and pass any replacement legislation in a way that – in combination with the repeal legislation – reduces rather than adds to the overall debt now and in the future.ConclusionThe new Congress and president have made clear that Obamacare repeal and replacement is a top priority. Any legislation to significantly modify or replace the ACA will have numerous implications, including many fiscal in nature.Certainly, repeal and replacement legislation should be designed and evaluated based on its impact on coverage, premiums, and economic growth. But it is especially important that policymakers focus on the impact of repeal and replacement on health care cost growth and the overall federal budget.As we argued around the passage of the ACA eight years ago, health reform is an iterative process that requires time and vigilance to ensure that long-term goals are being met.The national debt continues to rise unsustainably, and that is in part a direct result of the unsustainable nature of U.S. health care costs. If policymakers want to repeal the ACA, they need to do so in a way that would improve the debt’s trajectory, shore up Medicare, and spur further economic growth.For more information, contact Patrick Newton, press secretary, at newton@crfb.org.

Committee for a Responsible Federal Budget

1900 M Street, NW

Suite 850

Washington DC 20036 United States -

- CBO Predicts 18 Million Uninsured, Higher Premiums In First Year After Obamacare Repeal And Delay

- Why Republicans Can’t – and Won’t – Repeal Obamacare – Real Clear Health

- Trump promises his Obamacare replacement plan will cover all: Report – CNN

- Interactive Maps: Estimates of Enrollment in ACA Marketplaces and Medicaid Expansion – Kaiser Family Foundation

- Paul Ryan Faces (and Flunks) Healthcare Test – Rachel Maddow Show

- Obama Just Became The First Sitting President To Publish A Scientific Paper

- Local health care outreach program to Muslims ends with Ramadan – Chicago Tribune

- Obamacare Google Questions – How to Sign-up — Vox

- 2015 ACA Flyer

- Senator Ted Cruz Changes His Story on Obamacare – Ted-I-Am by Paul Begala

- Americans Are Warming Up to Obamacare – Bloomberg

- Obamacare Website Getting So Much Traffic It’s Surprising Experts

- How Your Health Insurance Company Can Still Screw You, Despite Obamacare

- Ari Melber highlights health coverage popularity – MSNBC

- Starbucks CEO Howard Schultz: Obamacare Is A ‘Net Positive’

- Trader Joe’s Proves That Obamacare Can Free Us From The Wrong Jobs

- Here’s how much people are paying for Obamacare – Vox

- Obama Keeps Foot On The Gas For Health Care Enrollment

- ACA Benefits in 10th District – redirects to tenthdems.org

- A Louisville Clinic Races to Adapt to the Health Care Overhaul – redirects to nytimes.com

- Choice of Health Plans to Vary Sharply From State to State By REED ABELSON Published: June 16, 2013 – redirects to nytimes.com

- Health care Myths debunked & quick facts.pdf – 48.3KB

- Health Reform Hits Main Street | The Henry J. Kaiser Family Foundation – redirects to kff.org

- IllinoisHealthMattersSM – redirects to illinoisheelthmatters.org

- Obamacare Depends on Math of Matt Saniie From Campaign Data Cave By Mike Dorning – redirects to bloomberg.com

- This is the link to the Small Business HC Wizard – redirects to business.us.gov

- timeliine for H.C. policy implementation-1.pdf – 58.7KB

- Washington Post 7-5-13 Ruth Marcus Opinion Writer The real hurdles in Obamacare – redirects to washingtonpost.com

- White House unveils Health Care Wizard to teach business owners about Obamacare – redirects to washingtonpost.com

-

An Historical Look…

ObamaCare Enrollment Numbers OverviewBy the end of open enrollment 2014 over 15 million Americans who didn’t have health insurance before the ACA was signed into law in 2010 are now covered, bringing the total uninsured adults in the US from 18% to 13.4%. During the year many dropped their plans, or didn’t yet renew them for 2015. As of January of 2015 the current uninsured rate is 12.9% according to Gallup (average from fourth quarter of 2014). The change is on par with projections, and is expected to increase each year.As of January 16th, 2015 7.1 million are enrolled in a plan through HealthCare.Gov and 2.4 million enrolled through state Marketplaces. This number spiked to 10 million total enrollments by February. Are also currently 10 million Medicaid sign ups and 3 million on the parents plan to date. This however does not give us a complete count of total enrollments due to ACA related provisions. Learn more about how to understand ObamaCare enrollment numbers. HHS originally projected 9.1 million enrollments by February 15, 2015 (the end of Open Enrollment).We won’t know exact enrollment numbers for each insurance type until well after folks have enrolled. What we do on this page is present the data we do have, analyze it and give you our educated estimates. Below you’ll find links to official reports and our analysis of that data.Let’s look at some quick facts on the ACA signups and the start our detailed look at what factors contributed to the current enrollment numbers.Enrollment Number Facts For Open Enrollment 2015

So far we know that 7.1 million (as of Jan 16, 2015) have enrolled in a plan on the federal marketplace HealthCare.Gov. That includes about 4.5 million auto-renews and renewals, plus new enrollments. Those numbers were 6.8 million (as of Jan 9, 2015), 6.6 million (as of Jan 2, 2015), 6.5 million by end of 2015.The above is only in respect to federal marketplace enrollments (HealthCare.Gov only). These enrollments don’t count the 14 state’s using their own marketplace (estimated at 2.4 million as of January 16th, 2015, you can also look at state-by-state breakdown by HHS), those who got covered through Medicaid and CHIP (10 million), young adults staying on their parents plans (3 million), plans outside of the marketplace, job based coverage, and more. Taking into account enrollment numbers so far, and the fact that the employer mandate begins this year, we could see a pretty drastic decrease in uninsured. We will have more detailed information as more reports come in.NOTE: Last year 8 million people enrolled in a marketplace plan, not everyone kept their plan, and not everyone who kept their plan reenrolled. The current grand total of federal marketplace enrollments was about 6.5 million by the end of 2014. The current goal for open enrollment 2015 is 9.1 million paid on HealthCare.Gov.You can find more information about the HHS report on December 2014 enrollment numbers for ObamaCare here or the latest enrollment number report here. By following the HHS blog you can get up-to-date reporting on federal marketplace enrollments and Medicaid.Our 2013-2014 Actions

OAKTON COLLEGE ENROLLMENT DRIVE 3/3 3/4 3/5 : The event was a big success! Thank you to Keith Moens, David Horwitz and Peg Lane for helping with Monday, Tuesday, and Wednesday shifts at Oakton College GET Covered enrollment drive. You helped refer MANY students to the enrollment table to get covered!

INDIAN TRAILS LIBRARY ENROLL TABLE: Thank you Linda Wayce for volunteering for AM shift and to Lou Hoppe for volunteering for the PM shift on 3/5/14. Thanks again to Renee Gladstone and Joan Brody for volunteering to sit at the Indian Trails Library Get Covered table on 2/22/14 and 2/25/14. Thank you to Tuly Rodriguez for volunteering to be our Spanish translator at the Indian Trails library shift 10-2 every Saturday from now untill the end of March!! You are heroes!Thank you to the 10 volunteers who have attended our ACA Get Covered phone bank at Panera. YOU are HEROES to all you call!!Thank you ~ Lou Hoppe – Data Entry, Callers: Jimmy Stewart (trainer) , Linda Waycie, Kathy Niekrasz, Joe Gump, Peg Lane, Herald Whyte, and Doug Blair. Antulia Rodriguez – Spanish translator who is a HUGE help.

February 11, 2014

ACA Day of Action Press Event – Mile Square Health Center in Chicago

Local supporters joined to hear from people in the community who are already benefiting from the law in order to help others learn how they can get covered.

Medill Published News Article: http://bit.ly/1b22mal

________________________________January, 2014 – Press Event at Chicago Temple followed by fliering at State & Washington, Chicago

November, 2013 – The team getting ready to “Get Talking During the Holidays” in Buffalo Grove, IL

October, 2013 – Hearing from the experts in Arlington Heights, IL

August, 2013 – Getting the facts in Palatine, IL

___________________________

[/orb-custom-list]